On Tuesday the Planning & Zoning commission discussed a request on behalf of a check-cashing business in Byram seeking to operate a stand alone ground floor storefront in a commercial zone.

Per Greenwich’s building zone regs, financial services are not allowed on the ground floor in Greenwich Business Districts and check-cashing is classified as financial services.

Attorney Casey O’Donnell represented the applicant, ‘Free Enterprise Partners LLC,’ who operate “Check Cashing Plus” inside the Byram Laundry at 6 North Water Street on the corner of Mill Street. The business is owned by Ellen and Rick Freeman. The property is owned by Stavros Karipides.

Back in 2012, the business was allowed by Greenwich P&Z to operate a kiosk inside the laundromat that was limited to check casing and Western Union money orders as accessory to the primary retail use.

Fast forward to today, more than 10 years later.

According to a Jan 26, 2024 letter to P&Z from attorney O’Donnell, Check Cashing Plus’s use has contributed to an underserved Greenwich demographic and small businesses, “bringing vitality to the local retail and services trade.”

He said the business had not generated any complaints over 10 years.

O’Donnell’s request is for the Commission reconsider the 2012 decision and either make a finding that Check Cashing Plus’s use is Retail or provide feedback to develop a text amendment for the check-cashing use.

“Check Cashers often serve small businesses with high cash-flow demands and consumers who are under-banked,” the letter said.

O’Donnell noted that while the definition of Retail was narrow, many uses, including laundromat were nevertheless considered Retail.

Because service-based businesses don’t fit easily into the existing Retail definition, O’Donnell suggested a change so that a “Retail Financial Establishment” might include check-cashing and be permitted on the first floor in CGBR and LBR zones.

O’Donnell’s letter said guiding principle 5 in the 2019 POCD talked about commercial areas contributing significantly to the community’s overall character and vibrancy, and specifically mentioned financial services as a leading industry.

During Tuesday’s discussion, O’Donnell brought up the commission’s concern that traditional office-based or bank-based financial services can be “an interruption to retail.”

“Underserved, underbanked communities have a much higher, more clear need to have non traditional banks,” O’Donnell said.

“You think we’re under served for banking in this community?” commissioner Yeskey asked.

“We have a substantial under-banked population,” O’Donnell said. “…contractors are typically under-banked. They have high cash flow needs. So they may get a check and have to make payroll that same day.”

Commissioner Nick Macri noted the decision letter from 2012 approved the continued use of the kiosk, but explicitly said, “no second branch or similar type operation would be allowed in the LBR or CGBR zone.”

“Bottom line. There it is,” Macri said.

Commissioner Arn Welles said check-cashing was clearly a financial transaction.

“To try and pretend it’s something else – I wouldn’t go that route,” Welles said.

“I totally understand the underserved community you are representing here. It’s huge,” said commissioner Mary Jenkins. “An enormous number of people don’t have a bank account, so if they have a check it might as well be a newspaper. I’m very sympathetic to that.”

But, she said, “The problem I have with Family Financial Centers is, then it starts talking about payday loans. Loaning money – you’re talking about more paperwork and more like a traditional bank. And tax preparation.”

“If all you’re talking about is classic money transmission service – prepaid cards, Western Union – I can get comfortable with something defined as ‘money transmission services business. But if we start talking about retail financial businesses, it begins to feel too much like a bank.”

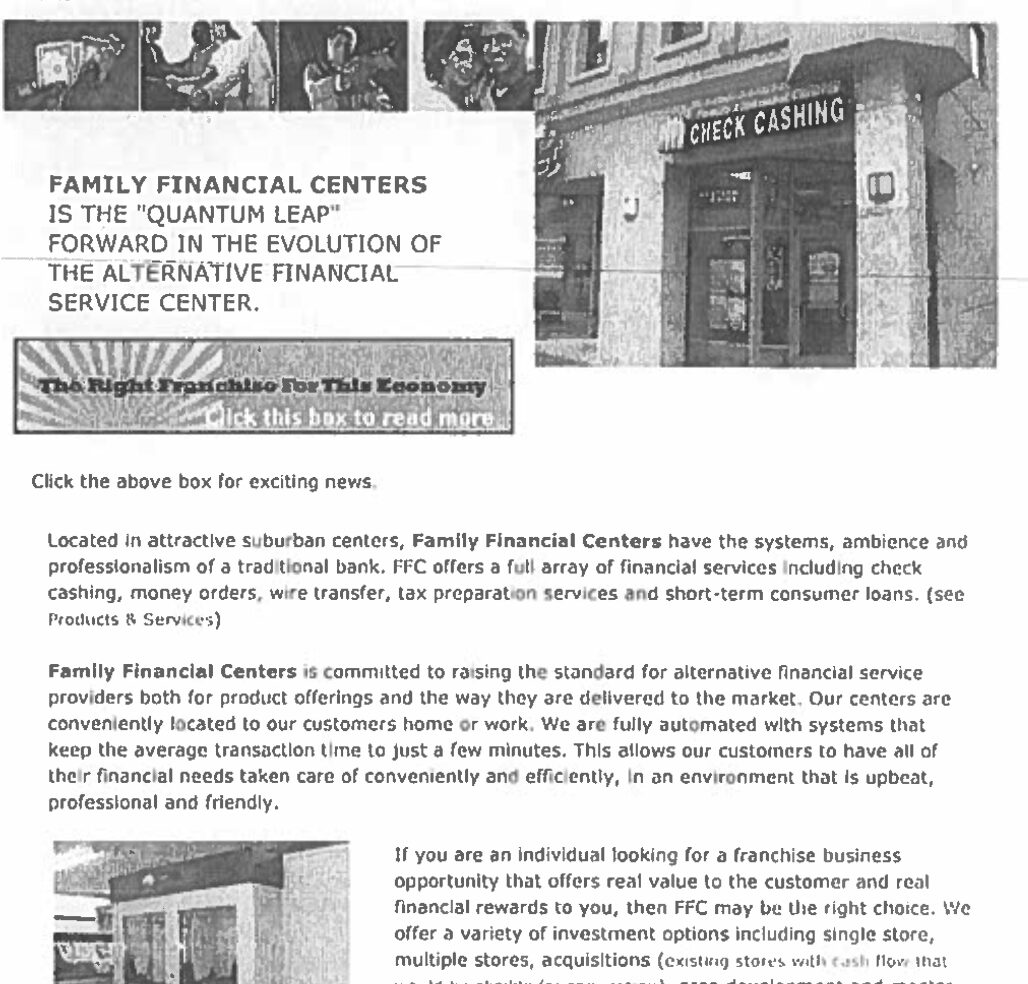

Jenkins’ comment referred to the applicant’s file that included the original materials from 2012, and information from Family Financial Centers, a franchising operation for check-cashing and short-term consumer loans, also referred to as “payday loans.”

From applicant’s file 2012.

“To me when you cash a check, it is a financial transaction. You are exchanging one form of currency for another,” said P&Z commission chair Margarita. “Both checks and cash are currencies.”

She noted that like supermarkets having ATM machines, she didn’t have a problem with the check-cashing as an accessory to a primary retail business.

“But we have to draw the line at financial uses on the ground floor,” she said.

Mr. Yeskey pointed out that stand-alone bars were not allowed in Greenwich.

“You have to have food,” Alban said.

Yeskey said this situation with check cashing was analogous.

“Family Financial Centers, LLC, is pleased to announce its newest location in Greenwich, Connecticut. This is the first location for franchisees and owners Rick and Ellen Freeman.

‘Locating their Family Financial Center within the local laundromat makes great sense,’ observed Paul Eckert, President and CEO of Family Financial Centers.

‘The Freeman’s are offering great and convenient services to the local market.'”

– 2011 post on the Family Financial Centers website titled, “FFC Adds Convenience to Laundry Day”

“Overall, this is the kind of use that I don’t think fits in the town. Stand-alone check-cashing and payday is notorious,” Yeskey said.

“Payday is illegal in Connecticut,” O’Donnell said. “I’ll save you that misunderstanding. And there’s no loans available. It’s a limited service.”

Alban said back in 2012, “the commission thought long and hard about protecting the streetscape, protecting how Greenwich looks and feels, the experience for pedestrians – all of those were considered.”

She also said check-cashing was indeed a financial service because the process involved changing one form of currency for another.

“There are services we don’t have in town that don’t exist, and we don’t really want – I’m going to, say, a strip club.”

She recalled that back in 2012 the commission was concerned that many banks wanted to have numerous branches and the commission was seeing a disruption in retail continuity. At the time Greenwich Avenue was not thriving.

Ms Alban said she’d like P&Z to seek a legal opinion.

The commission left the item open in order to discuss it further with the Law Department.